Barrick Gold has officially unveiled an offer to merge with Newmont Mining after several days of anticipation it would make a tilt for the gold rival.

The $US17.8 billion ($24.8 billion) all-share transaction would create the world’s largest gold company, with three Australian assets – the Super Pit and Boddington in Western Australia, and Tanami in the Northern Territory.

Barrick’s offer, however, represents a negative premium based on Newmont’s closing price on February 22. It also has the potential to derail Newmont’s $US10 billion plans to merge with Goldcorp, a deal the United States-based company believes offers better value than the Barrick tie-up.

Barrick chief executive officer Mark Bristow said the proposed merger with Newmont would unlock more than $7 billion of real synergies.

“The combination of Barrick and Newmont will create what is clearly the world’s best gold company, with the largest portfolio of Tier 1 gold assets and the highest level of free cash flow to drive future growth and support sustainable shareholder returns, run by a management team with an unparalleled record of delivering growth,” Bristow said.

A major portion of the synergies between the companies would be in Nevada, United States, where the deal would combine Barrick’s mineral endowments with Newmont’s processing plants and infrastructure.

Bristow said the proposed merger would secure Nevada’s position as the world’s most prospective gold region.

“Most important, it will enable us to consider our Nevada assets as one complex, which will result in better mine planning and fully realise the state’s enormous geological potential for all stakeholders,” Bristow said.

“Considered globally, the merger represents a radical and long-overdue restructuring of the gold industry, and a transformative shift from short-term survival tactics to the long-term creation of sustainable value.”

The Canadian company confirmed last Friday that it was reviewing the opportunity to make a takeover bid for Newmont following media speculation about a potential deal.

Newmont responded to the Barrick offer by stating it had a long history of evaluating potential transactions, and undertakes robust analysis and diligence on a continuous basis of acquisition opportunities.

“Newmont has previously reviewed and rejected potential combinations with each of Barrick and Randgold Resources, prior to their merger,” Newmont stated.

“Newmont’s proposed combination with Goldcorp represents the best opportunity to create optimal value for Newmont’s shareholders and other stakeholders.”

The company plans to fully evaluate the Barrick proposal and respond in due course.

Today we live in constantly evolving and technology-driven world. For mining operations specifically, adoption of digitalization is crucial for industry impact and success. Often overlooked by mining organizations because of its focus on smart products and engineering-driven manufacturing, Industry 4.0’s principles have much to offer the mining sector regarding:

Interoperability

Information transparency

Decentralized decision making

Technical augmentation

Among asset-intensive companies, better operational performance is the top reason for investments. The mining industry is no different mining companies must turn to Industry 4.0 and asset performance management implementation to improve safety, financial performance, and increase overall agility.

Read the E-book to learn how you can enhance your operations by capturing the Industry 4.0 payoff.

Liebherr is ready to strengthen the reputation of the R 9100/R 9150 excavators when its B versions of the machines arrive at Australian mines this year.

As the R 9100 has proved to be a worthy successor to the R 984 C excavators over the past seven years, Liebherr is convinced the B versions will add further benefits.

Liebherr delivered widespread improvements on the R 984 C with the R 9100 and R 9150, and set similar expectations during development of the new models.

The original versions have, however, provided a strong foundation for Liebherr to build on.

Liebherr launched the R 9100 in 2010 and the R 9150 two years later. Since 2012, the OEM has sold machines for operation in 21 countries over six continents.

The excavators have operated for more than one million hours at the mines, with a third of the machines recording more than 15,000 hours each.

They are used across operations for numerous commodities, including gold, coal, iron ore, copper, nickel and manganese.

Australian miners and contractors are amongst the users of the machines, including Blue Cap Mining, which operates two R 9150 excavators at gold sites in Western Australia and Queensland.

Blue Cap general manager Paul Allen says the R 9150 has many notable qualities that have made it suitable for the small hard rock operations where they are in use.

“We have seen both excavators perform well at different sites with different challenges,” Allen tells Australian Mining.

“Part of the reason we went for the 9150 was the specification and capacity of the machine, its hydraulic system and the additional power you are pulling in that unit – it has 565kW.”

Blue Cap pairs the excavators with haul trucks in the 100-tonne class, a match that been a strong fit for the designs of the pits at the gold sites.

Another key factor that helped the R 9150 stand out for Blue Cap was the technology Liebherr included on the machines, Allen continues.

“It was (at the time) more about some of the newer technology that Liebherr embedded around productivity and fuel efficiency,” he says.

“We are seeing around 15-20 per cent more efficiency out of this digger compared to some competition.”

With the success of Blue Cap’s R 9150 excavators, Allen has taken a keen interest in the updates incorporated on Liebherr’s updated models.

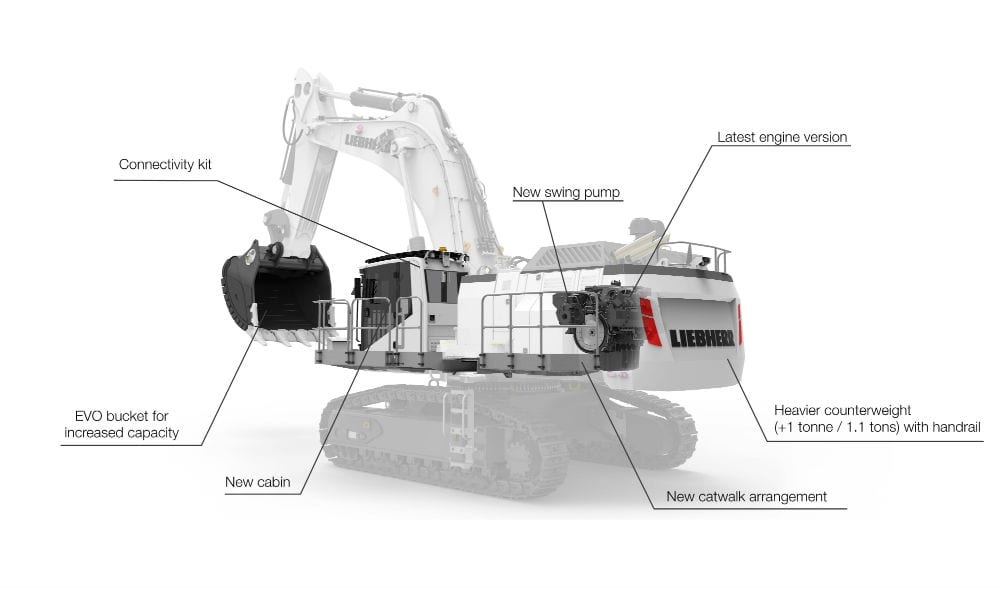

The B-version excavators were launched in January and the first machine in Australia will be received this month.

Liebherr senior product manager – mining excavators George Barturen backs the new excavators to drive productivity at mining operations, whatever the environment.

“Such systems are robustly designed and will be very well suited to the Australian mining environment from our extensive experience over the last five decades,” Barturen says.

“The B series machines, as was the R 9100 are suited to all mining and quarrying operators as the machine brings a competitive advantage regardless of the mined commodity with a reduced cost per tonne.”

Blue Cap’s R 9150 at the Red Dog site. image: Blue Cap Mining.

Stepping up operations

Liebherr’s updated hydraulic excavators have been developed to provide a step forward in performance and reliability, while lowering the cost per tonne.

Both models have received upgrades across the machine, including the latest generation of Liebherr’s D9512 engine, which offers an increased lifetime target of 15,000 hours, and other features that support maintenance efficiency.

The B versions include the exclusive EVO Bucket Solution, maximising loading capacity and ensuring optimal penetration efficiency.

With contoured sidewalls and augmented depth, the EVO Bucket has a 7.5m3 capacity on the R 9100 B and 8.8m3 and 9.6m3 on the R 9150 B, the latter being available on machines configured with a shorter boom.

The buckets match the excavators with the Liebherr T 236 truck, as well as other articulated and rigid trucks in the 50–100-tonne class.

Liebherr has positioned the R 9150 B directly between the 100-tonne and 200-tonne class machines with its bucket capacities. The R 9150 B begins to challenge the productivity of larger machines in the 200-tonne class with 12m3 buckets.

Barturen says incorporating the patented EVO Bucket design to the new machines is the most significant advance that increases productivity.

“This has brought about an increase in bucket payload with a reduction in bucket weight, whilst maintaining the same fast cycle time,” Barturen says.

“Additionally, the EVO Bucket for backhoe machines Liebherr is introducing several patented innovations together with machine functional control systems to provide the operator with semi-automatic functions increasing the overall efficiency and productivity of both machines.”

Barturen, a Liebherr employee since 1991, has worked closely with the company’s mining excavator team on the development of the B versions.

Alongside fellow Liebherr product manager Michel Runser, Barturen has guided the excavators through their final stages of development before launch.

“The main drivers in the development process were to improve the machine as a whole, enhancing machine safety, improving reliability and productivity KPIs and introduce operator comfort options, both active and passive.” Barturen says.

“The Australian mining industry drives continuous improvement of the machines through the different standards, guidelines and mining industry associations.

“Additionally, Liebherr has an internal global reporting system, which brings feedback directly into the factory from the field, speeding up the implementation and introduction of suggested improvements to suit the market, which is continuously driving improvement.”

Updated Liebherr engine

This series of Liebherr excavator was the first to introduce the OEM’s own diesel engines, a milestone reflected in the B versions. The R 9100 B and R 9150 B are equipped with Liebherr’s latest D9512 V12 diesel engine, which exists in Tier 2 and USA/EPA Tier 4 final version.

Liebherr Australia executive general manager, customer service, Tony Johnstone says the company’s service team has updated its skillset to support the new engine since its introduction.

Johnstone believes this has led to a new approach for the team, which has previously serviced and maintained engines from other OEMs.

“For us the challenge has been the development of our service technicians to be ready to work on the machines, understand the systems and be able to provide the best services that are required for customers,” Johnstone says.

“We’ve also had the challenge of upskilling our technical trainers so that we could train all of our service technicians in the Liebherr engine.”

Liebherr’s Australian-based technicians completed training on the engines in the company’s Switzerland engine factory certified training centre, with focus on control systems, maintenance and diagnostics.

In addition, customer training will be provided by Liebherr certified trainers at the new technical training centre at the Para Hills West facility in Adelaide.

The company has also ensured it has widespread availability of the unique service and maintenance parts for the engine.

“We had to stock appropriately for parts and for the future which we are working on now; we are enabling our remanufacturing centre to rebuild and run the D95 series engine,” Johnstone says.

“It has been a ground up approach because it was the first Liebherr engine in a Liebherr mining excavator.”

Liebherr’s preparation for the change of engine has the services team well placed to support the B versions once they arrive in Australia.

The R 9150 B will also be available in electric drive.

The updated features of the B version machines. Image: Liebherr.

Comfort and safety first

The B-version machines feature an upper structure that is accessible via a robust fixed ladder or 45-degree access stair in option. It integrates one large central platform equipped with slip resistant surfaces.

Liebherr has designed the new arrangement with wide catwalks to facilitate maintenance and to ensure comfort during operations.

“Included in the upgrade was the integration of hard safety systems – an improved catwalk on the left side of the machine, together with a handrail installation on the counterweight for added safety during machine and engine maintenance tasks,” Barturen says.

“Integration of HEPA filtration of the operator cabin is available should the requirement be needed.”

The cab, updated with improved ergonomics and operator attenuation, provides the ideal working platform and optimal comfort for operators.

Liebherr’s resiliently mounted cabin on ISO mounts reduces vibration, while a new cabin interior liner provides a two decibel decrease in noise levels in the cabin for the operator.

Technology advances

Liebherr has shown its awareness of modern connectivity needs, equipping the B version machines with GSM data transmission, together with the ability to transmit on customer site networks to provide operating parameters, error codes and machine faults.

Machine end users can access the data through the Liebherr Mining Data (LMD) platform, and generate custom reports to track and analyse machine data.

Barturen says the excavator product team focused on Liebherr’s six pillars of mining: safety and environment, productivity, efficiency, reliability, customer service, safety, and environment when enhancing the machines with technology.

“Improvements to the machines’ operating systems provides enhanced machine operational efficiency. Together with the integration of machine data management and analytics, the B series will enable customers to increase the effective utilisation of the machine in lowering the cost per tonne,” Barturen says.

“Customer service is enhanced by on board systems for the management of the machines’ maintenance and reliability interfacing with the Liebherr developed Troubleshoot Advisor.”

The data collected by the connectivity kit is recorded in a worldwide database for processing and assessment by Liebherr.

NRW Holdings head Jules Pemberton says the company has received “positive engagements” from clients following its acquisition of two RCR Tomlinson companies.

The contractor, which today reported it had finalised the deal, announced last month that it was purchasing RCR Mining and RCR Heat Treatment for $10 million as part of RCR Tomlinson’s ongoing selloff after entering administration last year.

Despite RCR’s financial failure, Pemberton noted that its purchase had received a positive response from NRW’s clients due to RCR Mining’s reputation as a “leading original equipment manufacturer.”

“This acquisition delivers a complementary business to NRW and aligns with NRW’s strategy to broaden the service offering to Tier 1 clients at a time of improving market sentiment,” Pemberton said.

“[Our clients] recognise the quality of the RCR Mining Technologies business and its people, together with the benefits the combination with NRW brings to their project objectives.”

RCR’s mining and heat treatment businesses’ locations in Welshpool and Bunbury, Western Australia, in addition to a facility in Victoria, have all been kept in the buyout, and around 300 staff have received employment offers with NRW.

Other administrative sales of RCR Tomlinson businesses so far include EGL’s purchase of the company’s energy division for $3 million and John Holland’s purchase of RCR O’Donnell Griffin’s rail business for an undetermined price.

BHP’s growth aspirations to significantly increase copper output at Olympic Dam have been recognised by the South Australian Government with major development status.

The miner hopes to expand Olympic Dam’s copper production by 75 per cent, from 200,000 tonnes per annum to 350,000 tonnes per annum.

BHP is progressing its growth studies for the expansion and will seek board approval for a capital project in mid-to-late 2020.

The South Australian declaration is, however, an important milestone for BHP as it considers an investment potentially as high as $3 billion for the project.

It is the first step in a state and federal process that includes assessment of potential social, economic and environmental impacts associated with an increase in mining and production at the site.

Olympic Dam asset president Laura Tyler said BHP was aiming to achieve stable operations and sustainable growth at the mine through a staged and capital-efficient approach over the long term.

“Olympic Dam is a world-class resource with the potential to deliver value to BHP and South Australia for many decades to come, especially given our positive outlook for global copper demand,” Tyler said.

“We are pleased the South Australian Government has declared Olympic Dam’s growth plans a major development, recognising our significance to the state.

“Our team continues to refine the scope for targeted underground development in the Southern Mine Area, strategic investment surface processing facilities, new technology and supporting infrastructure.”

The proposed expansion of Olympic Dam would be the latest in a series of projects for BHP at the site in recent years.

BHP invested more than $600 million into the copper operations during the 2018 financial year, with focus on underground infrastructure and above ground processing operations.

South Australian Minister for Energy and Mining Dan van Holst Pellekaan said the latest $3 billion expansion proposal could potentially create up to 1800 construction jobs with an additional 600 ongoing positions in operational roles.

“Olympic Dam is already the state’s largest mining operation, providing jobs, investment and royalties for South Australia,” he said.

BHP produced 65,000 tonnes of copper at Olympic Dam in the December half year, a 20 per cent increase on the previous period when a smelter maintenance campaign took place.

Aluminium is displacing classic steel, the shortage of skilled workers is to be compensated for by progressive automation, and environmental protection is increasingly becoming a priority – this is only a small part of the topics that will dominate the foundry industry this year and in the years to come. We present you with five trends that you should keep an eye on this year.

1: Aluminium instead of steel

Ever more products are produced with the material aluminium. There are numerous reasons for this: The automotive industry is just as pleased as the avionics sector when it comes to lighter components. However, the stability of aluminium is also a major factor. In mechanical engineering, this material is also used for mechanically demanding tasks.

In 2017, approximately six per cent more aluminium was produced than in the previous year. The higher price of the material becomes an ever smaller argument against this metal: The price of the finished product decreases due to advanced manufacturing methods and state-of-the-art machinery. Raw material prices have been comparatively high for years, but they are not affected by as many fluctuations as metal.

Fewer and fewer people are working in the foundry industry. Harsh working conditions and falling training figures suggest further declines. In order to remain competitive, companies rely on semi-automated or completely autonomous systems to maintain or even increase their production.

By no means does this lead to further job cuts. Quite the opposite: Employees are able to invest more time in designing or testing instead of pressing buttons on machines, transporting raw materials or filling molten metal at high risk. At the same time, this increases the interest of younger generations to get involved in the design or the development of the foundry industry.

3: Digitisation and Industry 4.0

Sensors, linked machines and smart controls have no fear for the foundry either: Numerous production sites are already centrally connected. Not only foundries, but also customers and potential clients benefit from the data. Processes can be optimised with big data and possible bottlenecks and errors in the system can be detected at an early stage. Manual adjustments in the operating procedure are less necessary.

New technologies like virtual reality help companies to present themselves to the outside world. Thus, a virtual tour of the production halls becomes possible for everyone. Safety concerns are no longer necessary – furthermore, a presentation of the company is possible everywhere. Thanks to augmented reality, technicians can easily adjust or repair machines with a superimposed virtual image. Also virtual learning becomes easier with the new technologies. Meanwhile, numerous CAD programmes can also be used by way of 3D glasses to make prototyping more efficient.

Foundries are considered to be amongst the most energy-hungry industries in Germany. The plants, which are often fed by coal, use around 16 per cent of the total electricity produced in Germany and 12 per cent throughout Europe. A study by the Federal Environment Agency proves that the majority of foundries could get their energy requirements from renewable energies. For this, however, energy storage devices are necessary that can meet the enormous requirements for continuous day-night operation.

Through the use of more efficient casting moulds, fewer raw materials are required, which also do not need to be transported. The energy requirement can be further reduced by using more efficient furnaces in order to make the entire production process more environmentally friendly.

Particularly for smaller cast products, things could change soon: More and more 3D printers are managing to deal with metals. Selective laser sintering (SLS) applies metal layer by layer in order to produce small components cost-effectively, quickly and more accurately than with conventional processes. Depending on the individual application, additive manufacturing offers various sizes ranging from half a cubic metre to entire warehouses that can be converted.

The innovative technology is already being used in projects that require only a small quantity of the final product. Structures, which would not be possible in normal casting, pose no problem for additive manufacturing either. For large quantities and parts with larger dimensions, not much will change for the time being.

The Environmental Group Limited (EGL) has secured a deal to purchase RCR Tomlinson subsidiary RCR Energy Service.

Melbourne-based EGL is dealing with the beleaguered engineering group’s administrator McGrathNicol to make the acquisition, which should be completed within the next week.

RCR Energy Service’s primary focus is on commercial gas and steam boilers, as well as thermal oil heaters and hot water heaters.

Perth-based RCR Tomlinson made headlines last November with the announcement of its administration due to insurmountable money problems, including around $630 million in debts.

The company saw a massive 60 per cent share wipe out in August last year and by the time of its administration its value hovered around 85–87 cents, down from $2.12 at the end of July.

In particular, the company suffered severe financial issues related to several failed solar farm investments — two Queensland solar projects saw a combined write down of $57 million, for example.

Despite this, EGL has cited RCR Energy Service’s “strong track record of profitability” as an attractive quality of the acquisition.

The company generated $21.5 million in sales and $1.5 million in earnings before interest and tax (EBIT) in the 2018 financial year.

RCR Energy Service’s senior management team will transfer to EGL once the acquisition is complete and the company will operate under the name Tomlinson Energy Service.

“EGL will continue to pursue new growth and acquisition opportunities that fit our environmental platform,” EGL chairman Lynn Richardson said.

“This will provide existing and new shareholders with the benefits of investment in a company committed to reducing pollution and the effective use of world resources.”

EGL did not reveal the cost of the acquisition at the request of McGrathNicol, but this information should be made available by the end of January. The acquisition will be funded by EGL’s existing debt facilities.

CFG Alliance is planning to construct a steel plant in Whyalla, South Australia, which will be the largest in the western world, according to company chairman Sanjeev Gupta.

Gupta announced the new project, Next-Gen Steel, alongside Prime Minister Scott Morrison and leader of the opposition Bill Shorten at a press conference in Whyalla on December last year.

“This is the turnaround state, and this is the comeback city in Australia when we’re talking about Whyalla,” Morrison said.

The project will create a new steel plant for Whyalla capable of producing 10 million tonnes a year.

Gupta also announced that the existing Whyalla steelworks would also be transformed through a $600 million investment into a 1.8 million tonnes a year steel producer.

GFG Alliance purchased the steelworks in 2017, saving hundreds of jobs in the process.

The company signed two contracts with Danieli and CISDI Engineering for the development of rail and structural heavy section mill and a pulverised coal injection (PCI) plant respectively over the next three years at Whyalla.

“The transformation will vastly improve the operations, financial and environmental performance of the operations, paving the way for Whyalla to become an enticing, global hub for innovative industry,” Gupta said.

The creation of the new next-gen steel operation with a capacity of 10 million tonnes a year (and the infrastructure to eventually double that capacity) and the upgrades to the current Whyalla operation is expected to increase the town’s population fourfold to around 80,000.

“This is a major boost for our long-term outlook and gives Whyalla City Council and other industries and businesses more confidence to be able to plan for the future,” said Clare McLaughlin, Whyalla mayor.

“The plant will also have state-of-the-art environmental controls, which is yet another positive for the community on top of the financial investment and job creation.”

Australian is seeing continued strength in construction applications, with 2,210 new projects entered in the country’s construction work pipeline in November 2018, with a combined worth of $25 billion – nearly double the three-year median value.

Infrastructure projects continue to dominate new project work in both quantity and value, although apartments and units are a close second for quantities of projects, according to CoreLogic’s latest Cordell Construction Report.

“The number of new construction projects entering Australia’s pipeline was just below the yearly high of 2,292, which was recorded in October 2018,” said James Shang, CoreLogic commercial research analyst.

“Although the total estimated value of new projects is approximately 16 per cent lower than the yearly high, it’s a strong indicator of continued strength in construction applications.”

A stand-out infrastructure project is the Aerotropolis project in Western Sydney, which is described as a ‘game-changer’, the project has an estimated cost of $8 billion, accounts for 50 per cent of the total new project applications in NSW for November and is expected to create 200,000 new jobs.

Whilst the number of new project applications is strong, the picture for projects further down the pipeline and actually moving into construction is less positive. These projects have fallen for a third consecutive month – the impact from a tightening credit environment clearly extending beyond the residential market.

“The estimated value of projects shifting into the construction stage during November was just over $2 billion,” Shang said.

“Whilst this figure is 53 per cent higher than the recent low (in October), it’s actually low when you factor in the strong level of activity in new development applications and when compared to historic levels too.”

Civil engineering projects accounted for 52 per cent of those projects moving into construction phase, whilst 54 per cent of value for projects moving into construction was thanks to the commercial sector. Mining held the highest median project value at $4.15 million.

For detailed industry and state-wide analysis, including project specifics, head over to the CoreLogic website.

In the early days of starting up my company Smart Books Online (SBO), I had no idea what I was doing.

Ok, I knew how to do the technical work, but I had no idea of what my ‘ideal customer’ looked like.

Accordingly, when it came to engaging new clients — I wasn’t fussy.

I needn’t care who they were, as long as they had money to pay me. I was just focused on sales to make payroll.

The challenge with business, particularly in the early phases of starting a new venture, is that it’s very difficult to say ‘no’. You take every meeting, every phone call, every bit of work that comes your way.

Even if you know in your heart and on paper that you might just break even or even lose money on a customer or project, you’ll say yes because you never know, it may lead to something bigger.

My newly formed habit of being a ‘yes man’ proved to be completely flawed as my business grew rapidly, from a revenue perspective anyway. Although sales were growing, we were losing money. Profit margins were getting squeezed due to discounting to win work.

Furthermore, due to misaligned client expectations, service declined. Customers were getting frustrated and were churning. As a result, I was losing more customers than I won. My financial and mental health was suffering as a result.

I was slaving away — 14 hours a day, 7 days a week, feeling overwhelmed and too busy to realize what I was doing wrong.

I mean, it could have been okay if I was profitable, but the truth was that I wasn’t. From a revenue perspective, I was crushing it. My business was consistently doing 20% month-on-month revenue growth (which is impressive growth for any business, irrespective of industry or size).

The problem, however, was while top-line revenue was growing, I was actually losing money. I was servicing unprofitable customers. I hadn’t designed a process on how to service our customers consistently, and profitably.

With the business spiralling out of control, something had to change.

My business partner and I spent a Sunday afternoon taking time away from the business and objectively analyzing it. We wore our ‘business owner’ hats and assessed our financial performance.

What we unearthed validated our gut feel assumption: Our business was a disaster.

The irony was that while we were supposed to be helping our customers with their firm’s financial performance, I couldn’t even do it myself.

“How ironic,” I thought to myself. I felt like an imposter.

Quickly snapping myself out of an emotional state, my rational brain got to work: Starting with a customer profitability analysis.

In our analysis, we discovered that the profit generated by the top 20% of our customers were absorbing the losses of the bottom 80%.

In other words, we were suffering because we were not selective about our ideal customers.

Being a yes person was killing our business.

Chances are, it’s also killing yours.

A practical guide to analysing the profitability of your customers

Here’s a step by step guide of how we undertook our customer analysis. I’ve tried my best to document all the steps, but if you get confused or lost — feel free to reach out.

Step one: Export a sales report

Export a sales report from your accounting system to a spreadsheet. Filter this data by customer name and dollar value of sales for the last 12-month period.

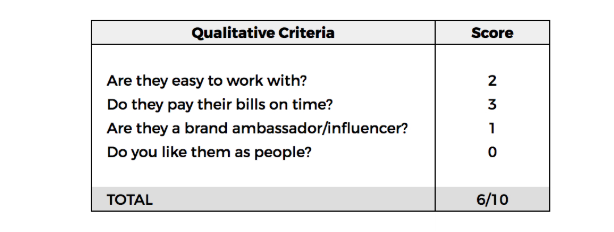

Step two: Ask questions

For each customer ask yourself the following questions:

Are they easy to work with?

Do they pay their bills on time?

Are they a brand ambassador/influencer to your product or service?

Do I like them as people?

For questions one, two and three, assign a score out zero to three (zero being terrible, three being amazing).

For the fourth and final question, make that it binary. Either a zero or one.

Tally your results, which will give you a qualitative score out of ten for each customer.

Example:

The process of allocating a score against each question helps you to assess your customers objectively. This quantification serves to eliminate any biases you have to your customers.

Step three: Calculate the direct cost

Calculate the average direct cost to service each customer and enter the value in a new column. You can allocate this off your timesheet data or project management system.

Step four: Calculate the gross profit

Calculate the gross profit earned on each customer by deducting the average costs to service each customer from the sales dollars.

Step five: Sort your customers by gross profit

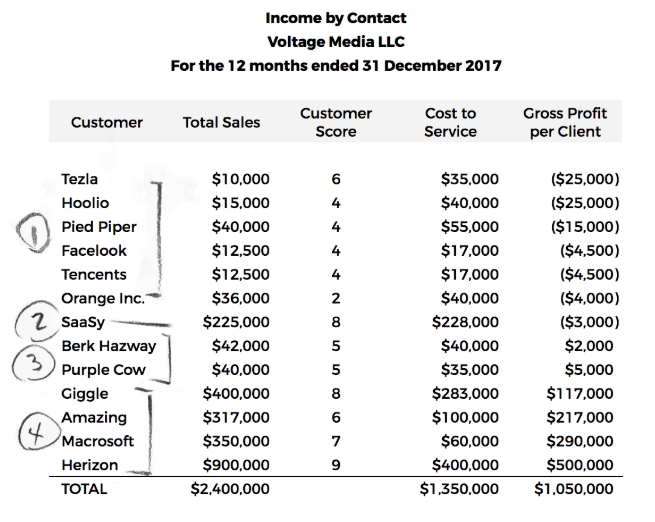

Filter the spreadsheet by gross profit of each customer and rank them per step two. The result is a list of your most profitable, desirable customers. They’re the ones you want to clone. And, at the bottom of the list, are the ones you want to cull.

The table above is a sample customer profitability analysis for a fictitious company called Voltage Media.

Here are the key observations:

The customers under note one are the customers you should fire. They rank low on the qualitative customer score, and they are loss-making. Fire them quickly.

The customer SaaSy under note two is less binary. This company brings in a lot of revenue and is ranked highly on the customer score. However, it is being serviced unprofitably. It’s fundamentally a great customer to work as it’s ranked eight out of ten, but ultimately, you cannot continue to service them profitably. In situations like this, dig deeper to understand why this client is unprofitable. Perhaps because you’re over-servicing them or not producing their work efficiently? Use this as a prompt to unearth the underlying issue.

The customers under note three are fence sitters. They rank in the middle from a customer perspective, and they generate a small profit to the business. You’re ok to hang on to these customers, but keep track of how they rank in the future.

These customers rank highly on the customer score and bring in the most profit to the business. Notice how the profit generated from these four clients carry the losses of the bottom half? These are the customers you want to replicate.

How to sack your customers

In the 24 hours that followed our customer analysis, I made several simple, but emotionally difficult decisions that literally changed my business. I took steps to fire the unprofitable 80% of my customers.

My outreach email was something like this:

Me: Hey customer, I’m reaching you to inform you of a few internal changes at our company. We’ve spent the last 12 months servicing our customers of all shapes and sizes, from startups to larger businesses. To date, we’ve been flexible to cater for all these different businesses as we want to help as many businesses as possible. As you can appreciate, being tailored for everyone does come at a cost. After reviewing our service offering and the associated fees, we are changing our prices. Your account will fall into the new package at $XX per month. I can appreciate this comes at a higher price, and this investment will ensure we’re able to continue to maintain our level of service.

Please reach out if you have any thoughts on the above. If I don’t hear from you in the next ten days we’ll assume you’re comfortable with the new arrangement.

Customer: I must say it is not an appealing proposition at all. As we have always been dealing with this issue fail to see what is different now and more surprising how it can double the monthly cost of the service you provide to us.

Me: I agree nothing has changed since engaging us, however our recent review showed we cannot service you profitably at the current rates. I hope you appreciate this doesn’t make business sense for us. I can refer you to a cheaper alternative if you wish. Let me know and I can make the introduction.

As expected, a handful of customers left us with and were happy to accept our referral recommendation to another service provider.

What we didn’t expect however was that the majority of customers accepted the price increases, and continue to be customers of ours today.

Giving your customers clear options to either pay a higher rate or, be referred to a cheaper alternative makes the decision binary, leaving no room for time wasting negotiations. Make the decision easy for your customers. They are busy people as well.

The net result was that we actually increased revenue because the price increase offset the churned, unprofitable clients. Making the decision cull these bad customers built a platform to maintain efficient and sustainable longer-term growth.

Although we had fewer customers, we were more profitable at a gross profit level, had more time and were most importantly, less stressed.

As business owners it’s easy for us to get stuck in the trenches, feeling overwhelmed and stressed with the state of your business. If you want to grow but not sure what to do start by reviewing your current customers.

Indeed, it sounds counterintuitive to sack customers in order to grow revenue and profitability.

But, to move forward, you need to start by getting your house in order.

This is an excerpt from Jason Andrew’s book, Stark Naked Numbers: Uncover Your Financials, Unlock Your Cash, and Unleash Your Profits, which launches on the 21st of January 2019.